ANZ will be ready to process mortgage holidays from Monday (30th March).

To compare how ANZ’s mortgage calculator compares to other banks check out this comparison article and guide to mortgage calculations.

Extract:

ANZ has assured customers that it is in good financial shape, and says its six month mortgage holidays will be ready to go by Monday.

Chief executive Antonia Watson says that borrowers will be able to start applying for the pause in payments from next Monday so long as their mortgage is in good shape, and they are up to date on their payments. The holiday will be for principle mortgage payments, with interest still accumulating in the meantime.

She also noted that the banking sector was more confident about facing this financial crisis as a result of the reforms brought in following the GFC.

“We’re not ready to hit the ‘go’ button, that will probably be about Monday,” Watson told RNZ.

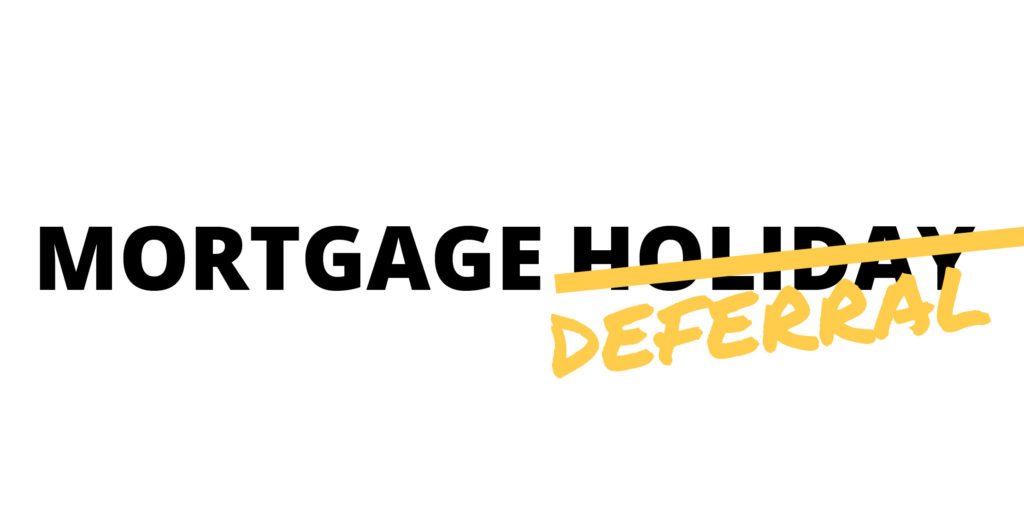

Please understand a mortgage holiday is actually a deferral. Essentially it looks like a pause on all payments with interest still accumulating. This means after the “holiday” your total mortgage will have grown due to interest payments being capitalised instead of paid. You will then have to extend the mortgage term or increase repayments from their current levels.

Alternative options to discuss with your adviser:

1. switch to interest-only (saves cashflow whilst ensuring your mortgage doesn’t grow)

2. consolidating high-interest debt (should be done anyway)

3. restructuring now to a longer-term (continue paying down your mortgage but with permanent lower payments)